Best No-Annual-Fee Credit Cards for US Consumers

Which one can you use in Canada?

Finding the right credit card doesn’t have to be expensive. In fact, many of the best credit cards in the USA now charge no annual fee, yet still offer cashback, rewards, travel perks, and solid security features.

If you’re looking to save money while maximizing your financial benefits, this guide breaks down the top no-annual-fee credit cards for US consumers as well as which one you can use in Canada.

Why Choose a No-Annual-Fee Credit Card?

A no-annual-fee card is perfect for Americans who want:

- Low-cost credit access

- Cashback or rewards without paying yearly charges

- A card to build or improve credit

- Backup credit without recurring fees

These cards offer excellent value, especially if you’re budget-conscious or want long-term savings.

How to start a business in Canada

Best No-Annual-Fee Credit Cards in the USA

Below are the top picks based on rewards, approval ease, security, and overall value.

1. Chase Freedom Unlimited

Best for: Cashback on everyday spending

What are the Benefits:

- 1.5% unlimited cash back on all purchases

- Bonus categories with higher rewards

- 0% APR intro offer on purchases and balance transfers

- Strong fraud protection

This is a top choice for Americans who want simple, unlimited rewards without worrying about rotating categories.

2. Discover it Cash Back

Best for: Rotating 5% cashback categories

Why It Stands Out:

- 5% cash back on changing categories (gas, dining, groceries, etc.)

- Unlimited Cashback Match for first-year cardholders

- No foreign transaction fees

- Great for students and first-time card users

The rotating rewards make this card a favorite for maximizing cashback throughout the year.

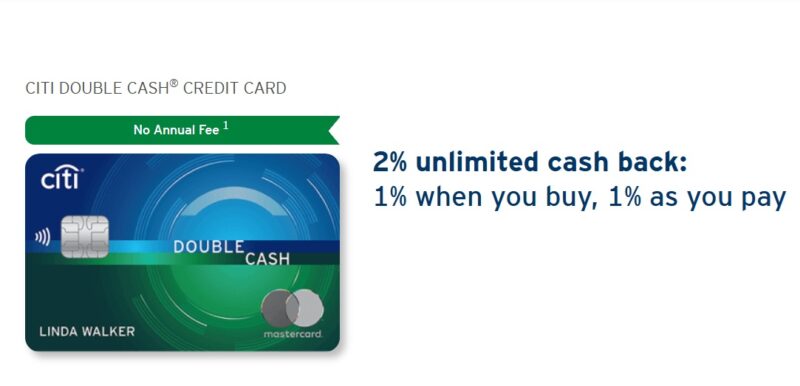

3. Citi Double Cash Card

Best for: Highest flat-rate cashback

What Rewards you will get

- Earn 2% cash back — 1% when you buy, 1% when you pay

- No categories to track

- Strong account security features

If your goal is consistent rewards on every purchase, this is one of the best cards in the USA.

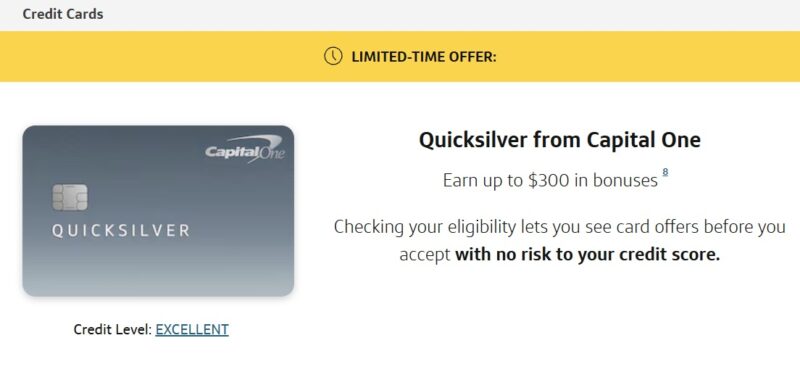

4. Capital One Quicksilver Cash Rewards Card

Best for: Simple and fast approval

What are the Benefits:

- Unlimited 1.5% cash back

- No foreign transaction fees

- Travel accident insurance

- Easy approval for average-to-good credit

A great all-rounder No-Annual-Fee Credit Cards for those who want quality rewards without complications.

5. Wells Fargo Active Cash Card

Best for: High cashback on everything

What are the Top Features:

- Unlimited 2% cash rewards

- Mobile phone protection when you pay your bill with the card

- Good redemption options (statement credit, gift cards, travel)

Ideal for Americans who want a premium reward rate without paying an annual fee.

Which No-Annual-Fee Credit Card is best for Canada

Here are some No-Annual-Fee Credit Cards that are pretty travel-friendly for use in Canada, because they avoid the extra 1–3% FX markup:

| Cards | Why It’s Good for Use in Canada / Abroad |

|---|---|

| Capital One Quicksilver Cash Rewards | No foreign transaction fees. Capital One states that none of its U.S.-issued credit cards charge this fee. It gives unlimited 1.5% cash back and has no annual fee. Reddit users also confirm it’s good for travel: “You won’t pay a transaction fee when making a purchase outside of the United States.” And the currency conversion is based on Mastercard’s daily rate, but there’s no extra “foreign-transaction fee” on top. |

| Other Capital One Cards | According to Capital One, none of its U.S.-issued cards, including all their travel and cash rewards cards, charge foreign transaction fees. So, if you want a no-fee card to use in Canada (or anywhere), many Capital One options are strong. |

Cards to Avoid for Canadian Spending

- From the No-Annual-Fee Credit Cards, there are a few that are not ideal for use in Canada because of foreign transaction fees:Wells Fargo Active Cash: This has 3% foreign currency conversion / transaction fee, per its account agreement.

- Chase Freedom Unlimited, Discover it Cash Back, or Citi Double Cash: These might have foreign transaction fees (or at least many of their variants do), so they’re less ideal unless you rarely use them abroad. Note that many Chase cards do charge a 3% foreign fee except for their premium travel ones.

How to Choose the Best No-Annual-Fee Credit Card

When selecting a card, compare the following:

- Rewards structure: Flat-rate vs category-based cashback.

- APR offers: Look for cards offering 0% introductory APR if you plan to make large purchases or transfer balances.

- Credit score requirements: Some cards require excellent credit, while others approve users with average or fair credit.

- Perks & protections: Mobile insurance, travel coverage, fraud alerts, and customer support matter.

What to Consider When Using a US Credit Card in Canada

- Acceptance: Most US credit cards (Visa, Mastercard, Amex) are accepted in Canada. However, in some smaller businesses or remote places, card acceptance can vary, so it’s good to have a backup payment method.

- Foreign Transaction Fees: When you spend in Canada using a US credit card, you’ll likely have to pay a foreign transaction fee if your card charges it. These fees usually range from 1% to 3% of the transaction amount. Some US cards do not charge these fees, if you’re choosing a card for cross-border use, try to pick one without FX fee.

- Currency Conversion: Even when you pay in Canadian dollars, your US card issuer has to convert that amount into USD. The “exchange rate” used includes a markup or conversion cost. Be careful about dynamic currency conversion (DCC) — if a Canadian merchant offers to bill you in USD instead of CAD, decline, because the converted USD amount may be expensive or have a poor rate.

- Chip & PIN vs Chip & Signature: Canada widely uses chip & PIN and many merchants may expect PIN verification. But US cards are often chip & signature, so at times you might sign instead of entering a PIN, generally this works, but there may be occasional friction depending on the terminal / merchant.

- Surcharging: Some Canadian merchants might add a surcharge for credit card transactions. But surcharges are regulated.

- Fraud / Dispute Protection: Using your US card gives you the same protections (fraud protection, dispute rights) under your US card’s terms. Always notify your US card issuer or bank before traveling or making large Canadian purchases, so they don’t flag your card for suspicious activity.

What you should do?

Keep in mind the following tips:

- For frequent use in Canada or abroad, stick to a Capital One card (like Quicksilver) as no foreign transaction fee is a big plus.

- Always pay in CAD when using the card in Canada (i.e., don’t accept to be billed in USD by the merchant), this avoids poor dynamic currency conversion rates.

- If you have multiple cards, you can keep a low-fee / rewards card for US purchases and use the no-foreign-fee card when traveling or shopping internationally.

- You can use your US no-annual-fee credit cards in Canada for most purchases.

- But unless the card has no foreign transaction fee, you’ll likely pay an extra 1–3% on each purchase due to currency conversion.

- If you plan to use the card often while in Canada (or for big transactions), picking a US card with no FX fee is a smart move.

- Also, always choose to pay in local currency (CAD) when making purchases, to avoid bad conversion rates via DCC.

Final Thoughts

The US market offers a wide range of no-annual-fee credit cards that deliver tremendous value without adding financial pressure. Whether you want simple cashback, great travel perks, bonus categories, or easy approval, there’s a perfect card waiting for you.

By choosing the right no-fee card, you can save money, build credit, and earn rewards, all without paying a yearly charge.